CASE FOR ENDOWMENTS: The Long and Short of Fundraising

Last year I wrote an article about a gathering of concerned university presidents in the early 1980s (See: “SOMETHING TO TALK ABOUT”). I attended as a Vanderbilt University graduate assistant at working in the education department and trying to come up with an idea for my dissertation—hopefully, one that would help to launch some kind of meaningful career.

Last year I wrote an article about a gathering of concerned university presidents in the early 1980s (See: “SOMETHING TO TALK ABOUT”). I attended as a Vanderbilt University graduate assistant at working in the education department and trying to come up with an idea for my dissertation—hopefully, one that would help to launch some kind of meaningful career.

Not many people plan to spend the better part of a decade in college with the goal of becoming a fundraiser. Neither had it occurred to me as a career choice. However, I was intrigued and astounded at what I heard from the college presidents in that meeting. As a result, my dissertation topic became an analysis of institutional outliers—university fund development programs that stood head and shoulder above the average. And my career launch eventually became Thompson & Associates, Inc.

So, here’s one more application to (what was for me) a career-changing meeting.

APPLICATION FOR ENDOWMENTS

In the late 1970s, and early 1980s, the inflation rate was a whopping 15% per year, and interest rates were even higher. Sheryl and I bought our first house around that time. Even though we had very good credit, the interest rate on our mortgage was 19%. The cost of borrowing was outrageous, and the cost of living (particularly the cost of educating) was rising faster than universities could raise tuition. An article in the journal for Council for the Advancement and Support of Education (CASE) had predicted that many private colleges would go out of business.

At the Vanderbilt gathering, one college president after another spoke about the dire consequences they faced—freezing salaries, postponing maintenance, and even laying off faculty and staff. It was as if a dark cloud had descended on the room—that is, until one president in turn made the following comments:

“We have a strong fundraising program and have also had some challenges. But this (financial crisis) has really not been our experience. We’ve made consistent efforts through the years to build our endowment. It’s been an ongoing priority for us.”

The president went on to explain, “Because of the high interest rates, this inflationary period has actually been our best friend financially.”

The cost of borrowing was outrageous, and the cost of living (particularly the cost of educating) was rising faster than universities could raise tuition.

When he had finished, for the next few moments you could hear a pin drop. Several other presidents seemed to clear their throat and commented that they too had endowments. However, it was pretty obvious that their respective institutions were not so endowed as to cause soaring interest rates to become their best friends.

In the early 1980s, institutions like Harvard, Princeton, and Stanford had diverse and sophisticated fund development programs, while smaller private colleges generally did not. Public universities were (for the most part) depositories where bequests would occasionally land. Very few public universities were proactively involved with foundation-sponsored estate planning services for their donors. Consequently, a gift to the endowment generally came as a surprise.

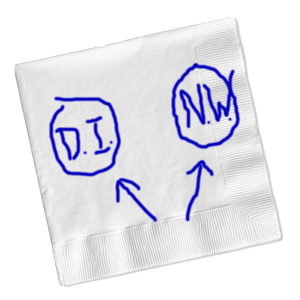

As part of my dissertation research on the best fund development programs, I went out to lunch with a fundraiser from Pomona College, one of the candidates for my list of best institutional programs. They had a long track record of success with both their annual fund and their endowment. The Pomona executive explained their success by drawing two circles on a McDonald’s napkin. In one circle he wrote “D.I.” and in the other, “N.W.”

“Eddie,” he said, “every nonprofit is asking donors to write a check out of their discretionary income (D.I.) But that request competes with going out to eat, going to the movies on Friday night, giving to the church, etc. There is strong competition for donors’ discretional spending. A big part of our success is that we have not only solicited gifts from discretionary income, but have consistently gone after gifts from net worth (N.W.).

TAKEAWAYS FROM PRESIDENTS’ MEETING

Having come away from that meeting with a sense of “WOW”, I jotted down several takeaways:

1) While high interest rates were negative for the students, the poor, and the middle class, they were in fact great for the wealthy. Imagine your net worth increasing 15% each year and doubling every five years. The wealthy (who tend to be strategic donors) regularly invest to own and rarely borrow to spend. The downside of inflation in the 1980s (i.e. higher costs of living) was not as significant for them as the upside of high interest rates. Likewise, an endowment in a season of high interest rates spews cash like an untapped oil well.

Over the last decade nonprofit leaders have begun a gradual retreat from that long-term perspective, evidenced by the ratio of major-gift to planned-gift executives they employ.

2. Donors are often less than enthusiastic about non-profit funding strategies. Typically, wealthy donors developed their giving capacity by accumulating assets over many years. That’s why many strategic donors are at odds philosophically with non-profits that operate with short-term perspectives of fund development.

Those college presidents from the early 1980s were fast learners. Over the next twenty-five years, institutions began placing a much greater emphasis on building endowments. However, over the last decade nonprofit leaders have begun a gradual retreat from that long-term perspective, evidenced by the ratio of major-gift to planned-gift executives they employ. The focus of non-profits is again becoming skewed toward current major gifts rather than endowments.

Lee Hoffman, President of Planned Giving Design Center, wrote in an April 10, 2013 post:

What if we lived in a world where nonprofits understood that they could not rely on future outcomes being the same as the here and now. Their approach to fundraising would be more balanced. The reduction of planned giving budgets and efforts over the last ten years may have been a fatal mistake for many.

2) Non-profit organizations need to simultaneously develop both current gifts and estate gifts. Many non-profits bifurcate (separate) these two aspects of their fund development efforts. When endowment and annual-fund efforts are comingled, the press for current wants and needs eventually wins out—the result being that emphasis on gifts to the endowment takes a back seat.

It’s much like the fuel mixture in an airplane engine. If the fuel-to-oxygen mixture is too rich or too lean, the engine under-performs. Far too much of either, and the engine simply shuts down. In the same way, overall fund development success requires that those piloting the organization constantly monitor and manage the mix of solicitations for current and long-term funding.

Eddie Thompson, Ed.D.

Copyright 2014, R. Edward Thompson

Spot on, Eddie! Balance is crucial for successful development programs.

I can’t say AMEN loud enough. It is vital for our leaders to understand these principals!